Every year, thousands of businesses face unexpected tax bills, penalties, and audits because they misunderstand their obligations regarding state and local personal property taxes.

Real estate taxes arrive as a straightforward bill. But personal property taxes place the reporting burden directly on the taxpayer. For companies operating across multiple jurisdictions, this self-assessment system creates a compliance minefield where a single missed filing can trigger cascading financial consequences.

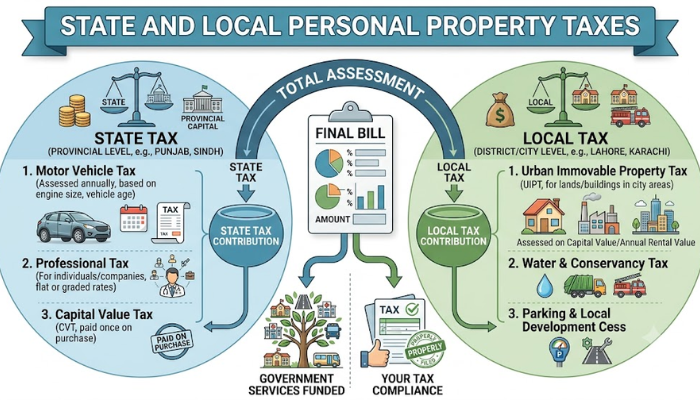

What are State and Local Personal Property Taxes?

In real property taxes, the government calculates what you owe. But, businesses must itemize every taxable asset (including machinery, equipment, furniture, and in some jurisdictions, supplies and inventory) then apply the correct depreciation schedules and jurisdictional rates.

For each asset, often across multiple filing jurisdictions with different rules, the compliance burden is substantial. Businesses must track:

- Acquisition dates

- Original costs

- Appropriate depreciation methods

This self-reporting mechanism is precisely where most compliance failures occur, not from intentional underpayment but from the sheer administrative complexity involved.

State and Local Personal Property Taxes Examples

The range of taxable assets catches many business owners off guard. Beyond obvious items like manufacturing equipment and office furniture, taxable property can include:

- Leasehold improvements

- Point-of-sale systems

- Consumable supplies (in certain states)

Some jurisdictions require reporting of expensed assets that fall below a company’s capitalization threshold – items already written off for income tax purposes but still subject to property tax.

Leased equipment presents another common pitfall: most jurisdictions require disclosure of all assets physically on-site regardless of ownership.

Understanding exactly what must be reported in each jurisdiction where your business operates is foundational to compliance.

A VAT number may also be relevant when determining the tax identification requirements for cross-border business asset reporting.

What is the Difference Between State and Local Personal Property Taxes and Real Estate Taxes?

| Features | State and Local Personal Property Taxes | Real Estate Taxes |

| What’s Taxed | Movable assets: equipment, machinery, furniture, computers, vehicles (varies by state) | Immovable property: land and permanent structures |

| Who Typically Pays | Primarily businesses; some states tax individual vehicles | Property owners (residential and commercial) |

| Filing Method | Taxpayer-active: business must self-report and file returns | Taxpayer-passive: assessor values property and sends a bill |

| Valuation Basis | Depreciation schedules, acquisition cost, fair market value | Fair market value determined by assessor |

| Geographic Scope | 36 states levy on businesses; 14 broadly exempt tangible personal property | Levied in all 50 states |

Which States Impose Personal Property Taxes?

According to 2025 Tax Foundation data,

36 states levy personal property taxes on businesses.

14 states broadly exempt tangible personal property from taxation.

Among states that do impose these taxes, 12 offer de minimis exemptions to reduce the burden on businesses with minimal taxable property.

Several states provide de minimis exemptions of 50,000 or more, effectively removing small businesses from the compliance requirement. These are:

- Arizona

- Colorado

- Idaho

- Indiana

- Michigan

- Montana

- Rhode Island

However, states like Kansas and Kentucky offer such low exemption thresholds (1,500 and $1,000 respectively) that most businesses remain subject to full reporting obligations.

Determining what is a financial institution under various state tax codes can also affect which exemptions and filing categories apply to your organization.

Who Pays State and Local Personal Property Taxes?

The primary filers are businesses that own tangible assets used to generate income. Typically, companies must file an annual rendition or return listing all reportable personal property, along with acquisition costs and dates.

For businesses operating across state lines, the complexity multiplies: each jurisdiction maintains its own

- Lien date

- Filing deadline

- Depreciation schedules

- Exemption rules

For instance, a multi-state manufacturer may face January 1 filing deadlines in one state, March 15 in another, and April 1 in a third – all with different reporting formats and asset classification rules.

Understanding what is tax yield can help businesses evaluate whether the cost of compliance in a given jurisdiction outweighs the tax liability itself.

Who is Exempt From State and Local Personal Property Taxes?

Exemptions generally fall into several categories.

- Household personal property used exclusively for personal enjoyment is exempt in virtually all jurisdictions.

- Tools used by tradespeople (plumbers, carpenters, auto mechanics) often qualify for trade-specific exemptions.

- Intangible property (stocks, bonds, and cash) is broadly exempt.

- Many states provide nonprofit and religious organization exemptions.

- The most impactful for small businesses are de minimis exemptions, which eliminate filing requirements entirely for companies whose total taxable personal property falls below a state-specified threshold.

These thresholds vary dramatically by state, making it essential to verify local rules.

The Bottom Line

Managing state and local personal property taxes requires proactive attention to jurisdiction-specific rules, filing deadlines, and exemption opportunities. The self-assessment nature of these taxes means the responsibility rests squarely on the business owner.

For businesses seeking professional guidance on such obligations, consulting with experienced tax professionals can provide both peace of mind and measurable savings.

L&Y Tax Advisors offers specialized expertise to help businesses develop compliant, cost-effective strategies for managing their personal property tax obligations.