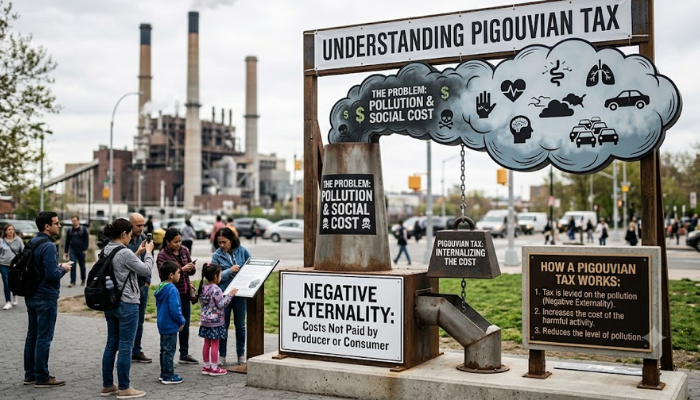

Markets do not always operate perfectly, especially when the production or consumption of goods creates unintended consequences for the wider public. When a transaction harms third parties who are entirely disconnected from the activity, governments often introduce a Pigouvian tax to regulate outcomes and restore economic balance.

What is a Pigouvian Tax?

A Pigouvian tax is a corrective monetary levy imposed on market activities that generate negative externalities. When validating corporate registration details or an official VAT number, analysts note that standard taxes raise revenue, whereas this specific mechanism internalises spillover costs to improve total Pareto efficiency.

What is a Negative Externality?

In macroeconomic theory, a negative externality represents an uncompensated, adverse by-product of an industrial or individual process. Common manifestations include:

- Ambient noise pollution

- Toxic industrial runoff

- Agricultural pesticide drift that inadvertently eradicates vital pollinators, forcing the public to absorb the associated economic costs.

What is a Pigouvian Tax Example?

Classic examples include:

- Carbon duties intended to mitigate environmental damage from fuel combustion

- Levies on tobacco products to relieve pressure on publicly funded healthcare networks

Such measures deliberately reposition monetary liabilities onto the specific economic actors responsible for producing or consuming the harmful items.

What is the History of Pigouvian Tax?

Pigouvian tax was named after the British economist Arthur Cecil Pigou. This conceptual framework was introduced in his 1920 seminal text, The Economics of Welfare.

Pigou argued that while industrialists pursue private marginal interests, they lack inherent incentives to address secondary societal harms, which he termed ‘incidental uncharged disservices’.

How Does Pigouvian Tax Work?

The policy operates by adjusting the private costs of production to reflect total societal costs. Administrative bodies within a specific tax district enforce these rates to realign market incentives, which encourages commercial entities to:

- Adopt cleaner methodologies

- Voluntarily reduce their aggregate output to a socially optimal equilibrium

What are the Benefits of Pigouvian Tax?

The primary advantage lies in the direct correction of market failures and the subsequent minimisation of broader public burdens. By penalising polluting behaviour, these duties:

- Encourage optimal resource allocation

- Improve general social welfare

- Generate secondary streams of public revenue that can fund public goods

What are the Drawbacks of Pigouvian Tax?

Critics, including Nobel laureate Ronald Coase, contend that externalities do not automatically cause structural market inefficiencies. Furthermore, calculating precise societal damage introduces significant epistemic challenges; overestimating external costs risks imposing regressive burdens that disproportionately diminish the disposable income of lower-income households.

Real-World Examples of Pigouvian Taxes

Modern policy incorporates these tools through carbon pricing systems targeting fossil fuel consumption. In addition, numerous European nations and Canadian provinces impose statutory levies on single-use plastic bags to curb marine degradation and discourage environmental waste while promoting reusable alternatives.

What is the Difference Between a Pigouvian Tax and a Sin Tax?

While visually similar, their underlying motivations diverge.

- A Pigouvian tax explicitly corrects negative externalities impacting external third parties.

- A sin tax targets negative internalities—self-inflicted harms like the personal health consequences of drinking spirits.

Often, questions arise about domestic assets, such as do you have to pay property taxes on land you own, which operate on entirely separate regulatory principles.

How Do You Calculate a Pigouvian Tax?

Accurate calculation demands that the exact duty matches the marginal external cost at the socially efficient output level. Mathematically, it fills the distinct gap between the marginal private cost and the total social cost. Though establishing this precise monetary figure remains notoriously complex.

The Bottom Line

Pigouvian taxes remain a key tool for internalising the costs of fossil fuels, tobacco, and sugar. They align private choices with social welfare. Though, precision and fairness are debated. The corrective instruments remain vital for managing contemporary public health and ecological challenges. Whether balancing these duties against subsidies or evaluating wider economic impacts, addressing market distortions ensures that the true societal expense of commercial enterprise is transparently accounted for globally.