Tax season brings a mix of confusion and opportunity. For many taxpayers, the goal is simple: reduce the amount of income subject to taxation to keep more of their hard-earned money. One of the most effective tools for this is the standard deduction. By comprehending what is standard deduction in tax, make informed decisions that simplify your filing process while ensuring you are not overpaying the government.

What is Standard Deduction?

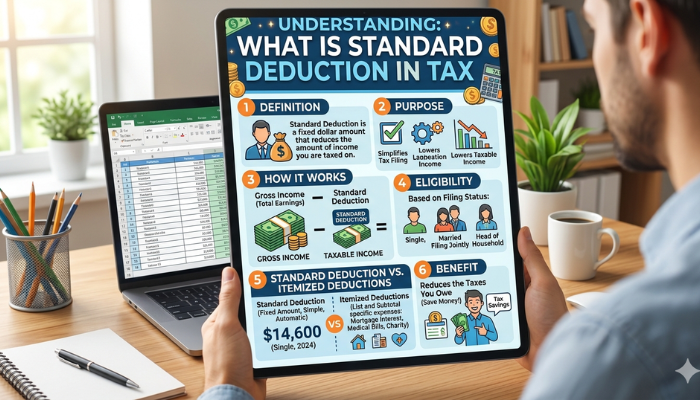

Standard deduction is a flat-dollar amount; the tax law allows you to subtract it from your adjusted gross income (AGI). It is a ‘no-questions-asked’ deduction. To claim it, you do not need to provide any receipts or proof of expenses. It serves as a baseline of income that is not taxed at all.

What is Standard Deduction in Tax?

Navigating the complexities of fiscal policy requires a clear grasp of what is standard deduction in tax and how it functions as a primary shield against higher tax bills.

Itemized deductions require tracking every charitable gift, medical bill, or mortgage interest payment. But, the fixed amount of standard deduction is adjusted annually to account for inflation.

For most filers, this route is the most efficient way to lower their tax liability. It is designed to ensure that individuals with very low income do not pay taxes. This also reduces the administrative burden on the average taxpayer.

When you apply standard deduction in tax, you essentially lower your ‘taxable’ income. This can sometimes even push you into a lower tax bracket. Monitor your VAT number or other business identifiers for corporate entities. But for individuals, this deduction remains the most straightforward path to savings.

What is a Standard Deduction Example?

To visualize the impact, imagine a taxpayer earning USD 60,000. If the set deduction for his/her filing status is USD 14,600, that person only pays taxes on USD 45,400. This immediate reduction happens without the need for complex record-keeping. This example proves that learning what is standard deduction in tax is essential for practical monetary planning.

How the Standard Deduction Works?

The system is built on a ‘whichever is greater’ logic. Compare the total of your potential itemized deductions against the fixed standard amount.

Most people find that the standard amount exceeds their specific expenses. Our professional tax advisor reviews highlight that this choice saves significant time during the preparation phase.

Exceptions and Important Considerations for the Standard Deduction

Not everyone qualifies for this flat deduction. For instance, if you are married, filing separately, and your spouse chooses to itemize, you are typically required to do the same.

Furthermore, knowing what is tax yield helps you realize that the deduction lowers the base. This directly influences the overall revenue generated by the tax system.

What Can I Deduct If I Take the Standard Deduction?

Generally, if you take the standard route, you cannot claim specific personal expenses like property taxes or home office costs. However, certain ‘above-the-line’ deductions can still be claimed. Consult with L&Y Tax Advisors to ensure you are capturing every available benefit.

Conclusion

Simplifying your tax return starts with a firm grasp of what is standard deduction in tax. Leverage this fixed deduction to bypass the headache of collecting piles of receipts while still capturing a significant reduction in your tax liability. Standard deduction remains the most popular and reliable method to protect your income and maintain monetary health.