Managing your money requires knowing how to calculate tax burden. Your tax burden is the amount of your wealth or income that is allocated to taxes. Knowing how much you pay is crucial for making wise financial decisions.

L&Y Tax Advisor presents how to calculate tax burden with 6 easy steps.

What is Tax Burden?

Most people think of their tax burden as whatever number appears on their annual return. That’s a starting point, but it’s not the whole picture.

Tax burden is the total weight of mandatory financial contributions an individual or business carries toward government revenue. That includes federal and state income taxes, payroll contributions, property taxes, and consumption taxes on the things you buy. Together, these don’t just reduce what you earn. They reduce what you actually keep. That distinction matters more than most people realise.

But here’s where it gets genuinely interesting.

Economists use a concept called tax incidence to reframe the entire conversation. Tax incidence not asks who writes the cheque, but who actually bears the cost.

A business may remit a payroll tax directly to the government, but if that cost gets passed on through lower wages or higher prices, the employee or the consumer is the one carrying the real burden. The legal payer and the economic bearer are often two different parties entirely.

Understanding your tax burden means accounting for all of it, not just the line items on a return. But the full reduction in disposable income across every applicable levy. It is the most honest way to measure what civic participation actually costs you in a given place, at a given income level.

And once you see it clearly, it tends to sharpen a lot of other financial decisions considerably.

Connect with our professionals for tax consulting services.

Tax Burden Example

There’s a misconception about tax brackets that costs people more stress than it costs them money, and clearing it up changes how you think about your entire salary.

Here’s a real example. Take a single taxpayer earning $95,000 a year. After maximizing standard deductions, their taxable income comes down to $80,000. At that level, they sit in the 22% marginal tax bracket. This is where most people make the mistake. They assume 22% of everything they earned goes to the government.

It doesn’t work that way.

A progressive tax system doesn’t apply your highest rate to your entire income. It applies different rates to different portions of your income, moving up through graduated tiers as earnings increase. The first portion gets taxed at the lowest rate. The next portion is at a slightly higher one. Only the income sitting at the very top of your range gets taxed at 22%.

Run the actual calculation across all those tiers and the total federal income tax liability comes to roughly $13,500. Divide that by the $80,000 taxable income and the real rate – the effective tax rate – is approximately 16.9%.

Not 22%. 16.9%.

That gap between the marginal rate and the effective rate isn’t a loophole or an estimate. It is simply how the system functions. Understanding it means you stop overestimating what you owe, start budgeting against accurate numbers, and make long-term financial plans based on what’s actually true – not what sounds true at first glance.

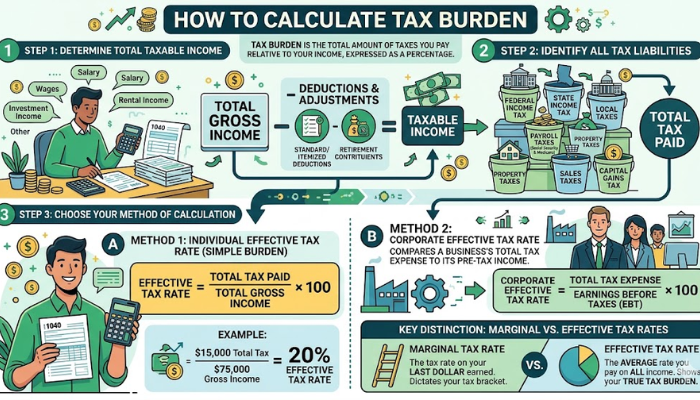

How to Calculate Tax Burden?

Determine Your Taxable Income

Finding your taxable income is the first step in figuring out your tax burden. For individuals, it comprises your:

- Wages

- Salaries

- Bonuses

- Investment income

- Other earnings

Subtract any allowable deductions from your total income to get your taxable income. Deductible expenses are:

- Medical bills

- Student loan interest

- Retirement contributions

You get your adjusted gross income (AGI) after deducting them.

Get your VAT number in the US.

Identify Applicable Tax Rates

Find out your income bracket’s current tax rates. In progressive tax systems, tax rates climb as income grows.

For instance, the tax system in the United States is tiered. Depending on your income, different parts are taxed at different rates.

Choose the appropriate tax rate for your AGI to calculate your income tax correctly.

Calculate Income Tax

To calculate your income tax liability, multiply your adjusted gross income (AGI) by the relevant tax rate. Remember this before looking at any credits or deductions that can further lower your tax obligation.

Read: Do strippers pay taxes?

Account for Deductions and Credits

Deduct any eligible credits and deductions from your income tax. Some examples are:

- Mortgage interest

- Medical bills

Dependents or educational expenses may qualify for credits

The taxes due can be significantly reduced by taking advantage of these credits and deductions.

Calculate Your Total Tax Burden

The sum of all taxes due is your overall tax burden. It also includes:

- Sales tax

- Property tax

- Income tax

- Other taxes relevant to your finances

You may have a better understanding of your total tax due by taking into account all forms of taxes.

Learn more about property taxes on new construction.

Calculate Your Effective Tax Rate

Determine your effective tax rate to see how your tax burden affects your finances.

To calculate this, divide your total taxes paid by your total income. Displaying the percentage of your income allocated to taxes helps you better comprehend your financial status.

How do I calculate my personal income tax?

If you’re wondering how do I calculate my personal income tax?, the process starts by determining your total gross income, which includes salary, business income, and any additional earnings. Next, subtract any allowable deductions such as retirement contributions, insurance, or other tax reliefs to find your taxable income. Once you have the taxable amount, apply the relevant tax rates based on your country’s tax brackets to calculate the total tax owed. You can also account for tax credits, which directly reduce the final tax payable. Finally, compare the tax due with any taxes already paid through withholding or advance payments to determine whether you owe more or will receive a refund. Understanding this calculation helps individuals plan their finances more effectively, avoid penalties, and ensure accurate compliance with tax regulations.

Personal Tax Burden Formula:

Tax Burden = (Total Tax Paid/Gross Income)*100

The Bottom Line

To learn how to calculate tax burden includes the evaluation of the above following steps. Doing so helps you better manage your money and clearly understand your tax liability.

Get our extensive tax consultancy services now!