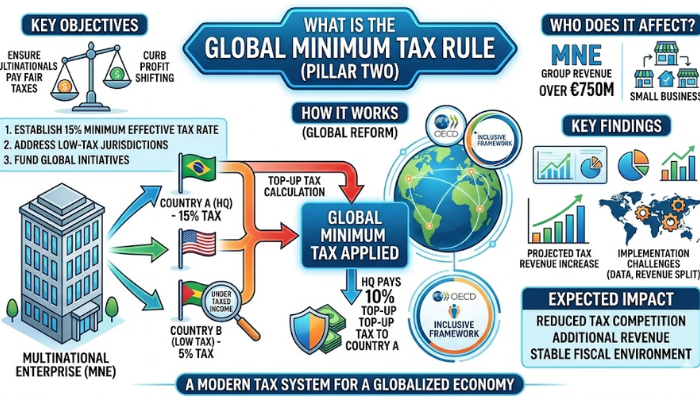

International taxation is currently undergoing its most significant transformation. The OECD/G20 Inclusive Framework has solidified the implementation of Pillar Two, commonly known as the GloBE rules. For multinational enterprises (MNEs) and large-scale businesses, comprehending what is the global minimum tax rule is a fundamental requirement for maintaining cross-border compliance and optimizing effective tax rates (ETR).

Who Proposed the Global Minimum Tax?

The GMT initiative was spearheaded by the Organisation for Economic Co-operation and Development (OECD). It was endorsed by over 140 jurisdictions. The framework was designed to address the challenges of a digitalized economy where profits are easily shifted to low-tax havens.

What are the Two Pillars of Global Minimum Tax?

The reform rests on two pillars.

Pillar One

Pillar One focuses on the reallocation of taxing rights for the world’s largest and most profitable companies based on where their customers are located.

Pillar Two

Pillar Two introduces the 15% minimum tax threshold to ensure a level playing field globally.

What is the Global Minimum Tax Rule?

The GloBE (Global Anti-Base Erosion) model establishes that if a multinational group with consolidated revenues exceeding €750 million pays less than a 15% ETR in any specific jurisdiction, a ‘top-up tax’ is triggered. This ensures that the global minimum tax rule acts as a floor. It prevents a ‘race to the bottom’ regarding corporate tax competition. The new ‘Side-by-Side’ package also introduced simplified safe harbors to decrease the reporting burden for eligible entities.

Global Minimum Tax Calculation Example

If a subsidiary in a low-tax country earns USD 10 million but pays only 5% tax (USD 500,000), the parent company’s jurisdiction would apply a 10% top-up tax (USD 1,000,000) to reach the 15% minimum.

What is the GMT Policy?

The policy mandates rigorous data collection across 100+ points per jurisdiction. Compliance involves the Income Inclusion Rule (IIR) and the Undertaxed Profits Rule (UTPR), which dictate which country has the right to collect the top-up tax.

What is the Main Purpose of GMT?

The primary goal is to neutralize the tax advantages of shifting profits to jurisdictions with little or no economic substance. By doing so, it stabilizes international tax systems and protects the tax bases of sovereign nations.

Is Global Minimum Tax Calculated?

Yes, it is calculated by comparing the ‘Covered Taxes’ paid in a jurisdiction against the ‘GloBE Income’ for that same area.

How is GMT Calculated?

To determine the liability, firms must aggregate all local earnings and taxes. If the resulting ETR is below 15%, the difference is multiplied by the jurisdictional profit to find the total top-up tax due.

The Bottom Line

Stay compliant in this shifting environment with a proactive approach to multi-jurisdictional reporting. L&Y Tax Advisors assists organizations in navigating these complex OECD mandates through precise impact assessments and strategic tax planning. As global authorities continue to refine what is the global minimum tax rule, having a dedicated partner ensures your business remains resilient against evolving regulatory risks.